The Only Holy Grail in Trading: Your Portfolio

No single trading system is the answer. 25+ live systems prove that portfolio construction is the only holy grail in systematic trading.

Welcome to the “Systematic Trading with TradeQuantiX” newsletter, your go-to resource for all things systematic trading. This publication will equip you with a complete toolkit to support your systematic trading journey, sent straight to your inbox. Remember, it’s more than just another newsletter; it’s everything you need to be a successful systematic trader.

Introduction:

Say you’ve spent a year or two building up your suite of trading systems. You’ve tested dozens of ideas, tuned parameters, refined entry criteria. Your your backtests look solid. You go live, and then they do exactly what most backtests do in the hands of a new systematic trader… underperform.

So you keep looking.

There has to be a better indicator.

A better parameter.

A better rule to add.

The equity curve on the next iteration is finally going to work. That search for the perfect system has a name: the holy grail. If you’ve been interested in systematic trading for any length of time, you know exactly what I’m describing.

I want to tell you something that took me 6 years of systematic trading and 25+ live systems to actually believe:

The holy grail DOES exist.

You’re just looking in the wrong place.

It’s not a system. It’s not an indicator combination. It’s not the perfect parameter set.

The holy grail in systematic trading (and the ONLY holy grail in systematic trading) is a diversified uncorrelated portfolio of many simple trading systems all working together. Once you understand why, you’ll stop trying to optimize your strategies to death in an attempt to create the perfect strategy, and instead start building something far more powerful.

Here’s what we’ll cover:

Why the single-system holy grail search is a dead end

The proof that a portfolio beats any single strategy

Why individually mediocre systems combine into exceptional portfolios

What my 25+ live systems actually look like across three markets

How to start thinking in portfolios instead of systems

Let’s jump in.

Everyone Is Searching for the Wrong Thing:

The reason systematic traders spend so much time hunting for the perfect system is completely understandable.

More parameters mean more precise fitting. A tighter filter means fewer bad trades. A more complex entry condition makes the backtest look smoother.

It genuinely feels like the path forward is to refine the single strategy until it looks good enough to trade.

The problem is that no single system is ever going to be good enough. Not because you’re a bad system developer, but because most systems on their own will never be good enough.

Every strategy has its issues and weaknesses.

Momentum systems crush it in moving markets and get destroyed in choppy or bear market conditions.

Mean reversion systems thrive in choppy markets and give it all back when a strong trend develops and you’re fighting it in the wrong direction.

Trend following systems grind sideways for years and then explode upwards once the markets start trending again.

No single approach works well in all market environments.

I know this from personal experience. Some of my individual systems have pretty rough stretches. Equity drawdowns that would make most people quit, and sideways choppiness that make you board to death.

But here’s the thing I’ve come to accept, that’s perfectly normal. Because no individual system has to carry the weight of the whole portfolio. We should be trading more than one system anyway.

We should be trading portfolios of systems. When you’re trading a portfolio of systems, the ugliness of one systems performance really doesn’t matter that much.

The Real Holy Grail: A Portfolio of Trading Strategies:

As you add uncorrelated return streams to a portfolio, risk drops dramatically while returns tend to stay relatively stable.

Having a portfolio of one strategy means your account is susceptible to all the lumps and bumps of that one trading system.

Having two systems that are somewhat uncorrelated starts to mute some of those lumps and bumps, canceling each other out.

Add 10 more uncorrelated systems and your portfolio equity curve starts to look like something pretty interesting.

With many uncorrelated trading systems working together, your portfolio equity curve starts to look like the equity curve of the one system you curve fit to oblivion trying to make the single holy grail system.

The only difference is, the portfolio is a combination of a bunch of lumpy and bumpy but real systems trading real edges. Where the single holy grail system is just a curve fit dream, overfit to noise and will never work in a live trading environment.

The closest thing we will ever have to a holy grail in systematic trading is a portfolio with multiple diversified uncorrelated systems working together to grind the portfolio higher.

There is no such thing as a secret indicator. I don’t have a proprietary market regime filter. What I have are multiple simple lumpy and bumpy uncorrelated systems working together in my portfolio.

The reason this is so powerful is that the backtested performance starts to become actually achievable going forward into live trading. Finding a single strategy that outperforms in all market conditions is nearly impossible.

Finding multiple simple systems that trade simple edges that all work well in different conditions, and underperform at different times, and then combining them together is the only holy grail in systematic trading.

Why Individually Mediocre Systems Create Exceptional Portfolios:

This is the counterintuitive part, and it’s worth spending time on.

Most systematic traders evaluate systems the same way:

Ensure the CAGR is high enough

Check if the max drawdown is low enough

See if the Sharpe ratio is interesting

Validate the equity curve is a beautiful straight line

etc.

If the system performance numbers aren’t high enough or the equity curve looks bumpy, the system goes through more fitting and more optimization until the numbers look right.

That framework is wrong.

In fact, an individual systems performance on it’s own does not matter that much, and we need to stop worrying about making a singular systems backtest as pretty as possible. How that system contributes to the entire portfolio is all that matters.

In fact, an individual system that loses money over the long term can still make your portfolio better.

Why? Because the only thing that matters for portfolio level improvements is whether the new strategy reduces overall portfolio volatility, dampens drawdowns, or smooths the returns.

If a strategy tends to make money when your other strategies are losing, it belongs in the portfolio; even if in the long run that one system never turns a profit on its own.

If you are deciding between two systems to add to your portfolio: a high Sharpe and a low Sharpe system. Almost everyone would lean towards adding the high Sharpe system over the low Sharpe system to the portfolio.

But remember to consider how that system adds (or subtracts) from your portfolio. A high Sharpe strategy that correlates with everything you already have does less for your portfolio than a mediocre low Sharpe strategy that zigs when everything else zags.

So stop asking yourself:

“What rule or parameter can I change to make this system better?”

And instead ask yourself:

“Does this lumpy and bumpy but real system improve my portfolio?”

What My 25+ Live Systems Actually Look Like:

I currently run 25+ live systems across US, ASX (Australian), and TSX (Canadian) equities. Here’s a rough breakdown by category.

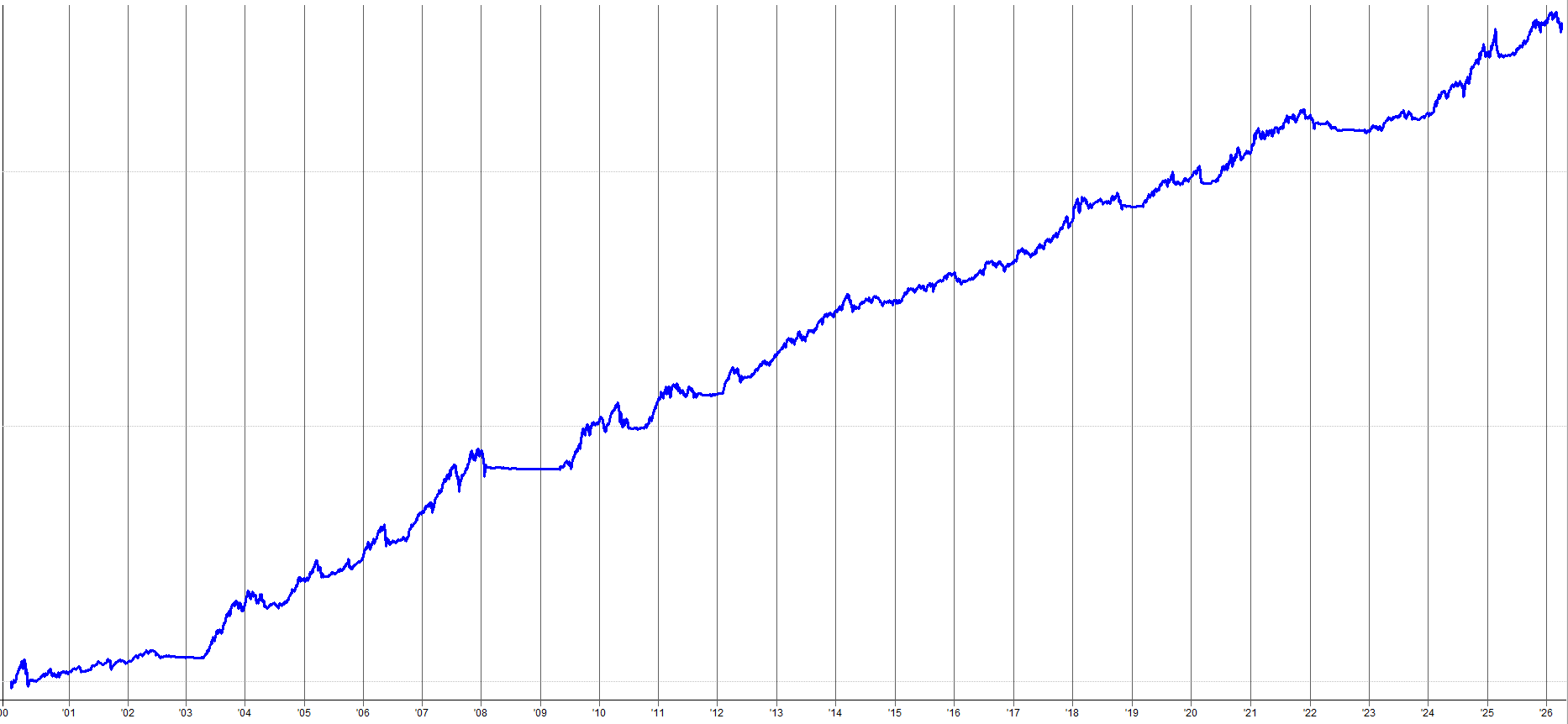

My momentum systems buy stocks that have been going up and bet they’ll keep going up. They work well in trending, risk-on environments. They can struggle in choppy markets when every breakout fails, and believe me, there are stretches where every single breakout fails. I run several variations of these momentum systems across different many universes. See the equity curve of all my momentum systems combined together below:

My trend following systems are similar to momentum but focused on price series specific trends rather than a cross sectional momentum measurement. These trend systems are generally slower-moving, typically longer holding periods. They provide some of the same benefits as momentum but with slightly different entry and exit timing. So even though trend and momentum are similar, having both add to the portfolio because they own different positions and enter / exit positions at different times. See the equity curve of all my trend systems combined together below:

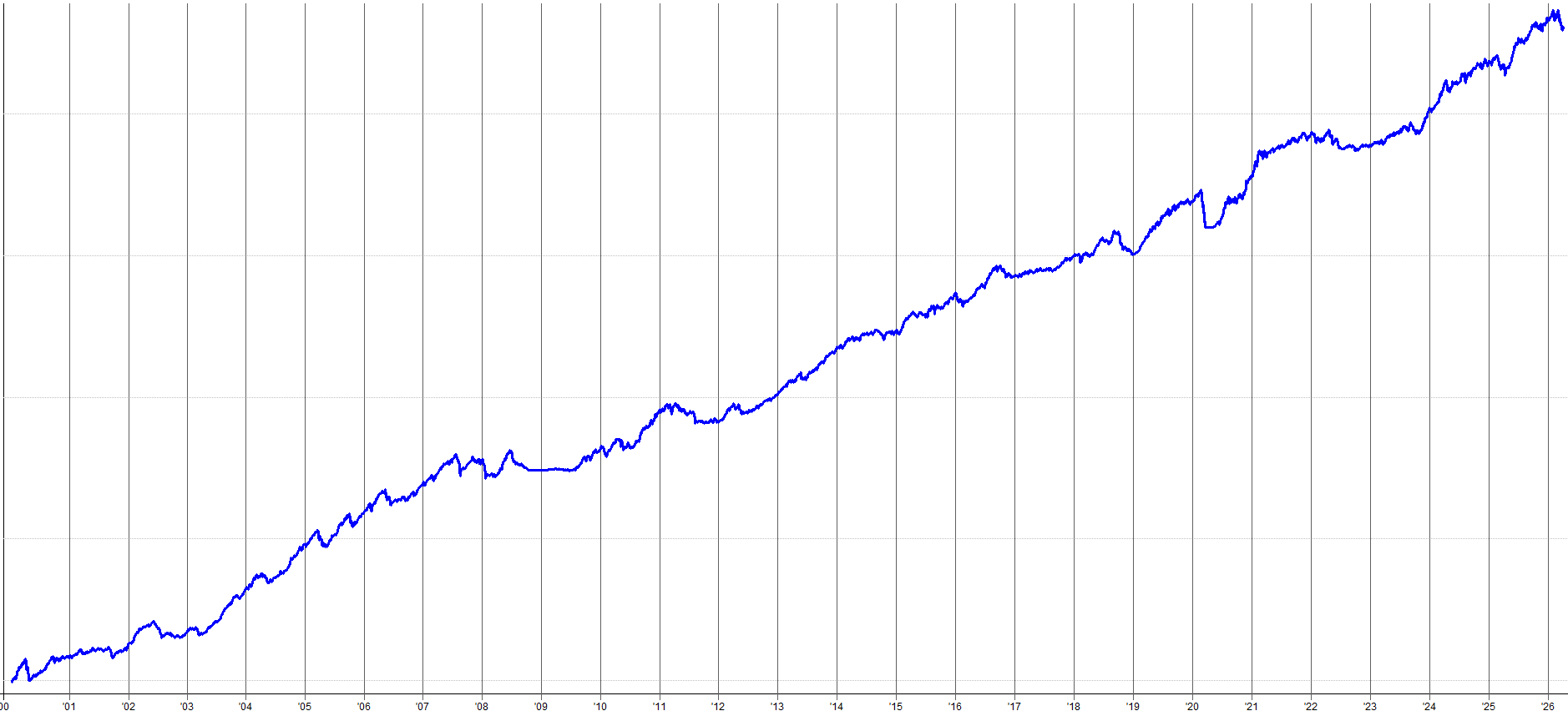

Then there are my mean reversion systems. These buy equities that have pulled back sharply, betting on a bounce. They work best in choppy, high-volatility markets, which makes them the natural complement to my trend and momentum systems. When my trend / momentum systems are struggling because the market is going sideways, my mean reversion systems are typically having a great quarter. See the equity curve of all my mean reversion systems combined together below:

And then there’s my hedging systems. I run a handful of systems specifically for hedging to portfolio during high volatility environments. When you look at the strategy equity curve on its own, it’s not that interesting. But as a portfolio component, it’s doing exactly what it’s supposed to: reducing drawdowns during the periods my long-only systems hate the most. See the equity curve of all my hedging systems combined together below:

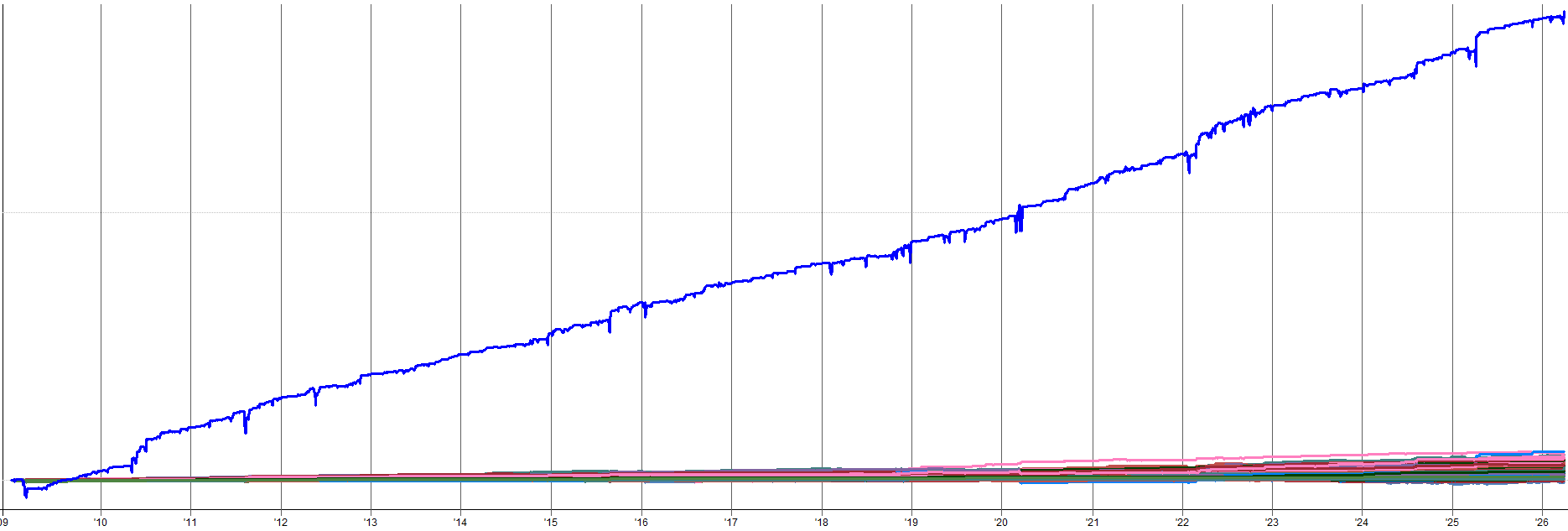

You’ll notice these system types operate on different mechanisms in different market conditions. Momentum and trend need upward moving markets. Mean reversion likes volatile, choppy markets (but still works well in trending markets too). Hedging systems perform well when equity markets are crashing. No single market environment hurts all of them at the same time.

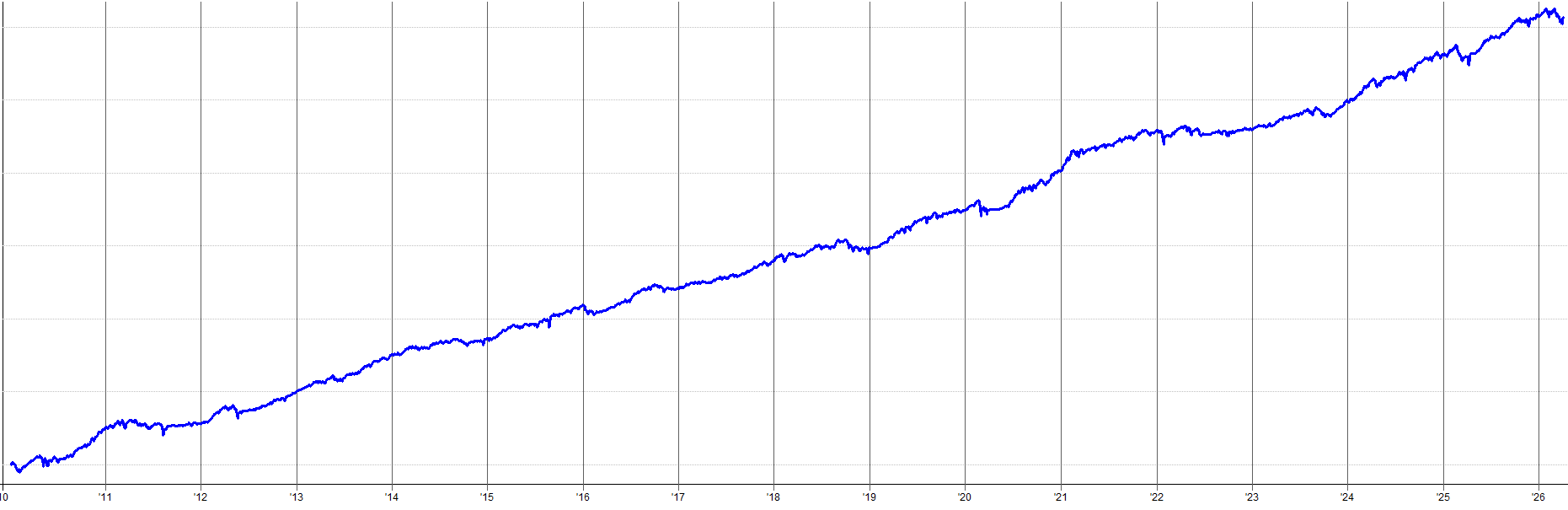

When you trade all of these system types together, the resulting portfolio starts to get interesting. The image below shows all my trend, momentum, mean reversion, and hedging system types combined together into the resulting portfolio.

For more details on my portfolio, with 25+ systems across three markets and their individual characteristics, check out the article below:

How To Start Thinking in Portfolios Instead of Systems:

If you’re early in your systematic trading journey, here’s how to reframe the way you evaluate new ideas.

The first mindset shift is to stop evaluating systems in isolation. The only question worth asking about a new system is whether it improves your portfolio.

A system with a Sharpe of 0.8 that is genuinely uncorrelated with your existing portfolio of systems will improve your portfolio more than a second mean reversion system with a Sharpe of 1.5 that correlates at 0.95 with the first one you already trade.

The second mindset shift is to think in strategy types, not individual strategies. Momentum, mean reversion, trend following, seasonality, event driven, hedging etc. Each system type responds to different market conditions. A complete portfolio should have many strategy types that behave differently from each other at different times.

The third mindset shift is how you evaluate backtests. Don’t discard a system because the standalone backtest numbers look mediocre. Discard it because your portfolio doesn’t need what that system offers. A mean reversion system with a modest Sharpe is still worth trading if you have ten momentum systems that all go sideways together during range-bound markets.

I’ve built my systematic trading portfolio over years, slowly diversifying across different markets, different system types, different timeframes, etc. Each system on it’s own is meh… but the combined portfolio isn’t half bad.

Conclusion:

The holy grail in systematic trading is real. It’s just not where most people are searching for it.

No single system is going to be perfect. Not because good systems don’t exist. Because even the best individual systems still underperform at times. The trick is trading multiple uncorrelated, simple, lumpy and bumpy equity curve systems together in a portfolio.

Shifting to this portfolio level mindset and implementation is the only reason I’m able to keep trading through drawdowns that would otherwise cause me to quit. I know I have so many uncorrelated systems working together that at some point, a few of them are going to start making money again and pull me out of that drawdown.

So, stop hunting for the perfect system and throwing away imperfect systems. Instead, start building a portfolio comprised of many imperfect systems.

Great stuff! I learned this from Ray Dalio 👍

What platform do you use for testing and deploying your strategies?