Market Effect Research: Turnaround Tuesday Effect

Turnaround Tuesday is a well known effect, but 99% of systematic traders capture it wrong...

Welcome to the “Systematic Trading with TradeQuantiX” newsletter, your go-to resource for all things systematic trading. This publication will equip you with a complete toolkit to support your systematic trading journey, sent straight to your inbox. Remember, it’s more than just another newsletter; it’s everything you need to be a successful systematic trader.

I recently launched a portfolio tracking website (updated daily) that tracks my systematic trading portfolio performance, along with many supporting metrics. You can check in on my personal systematic trading portfolio performance anytime here: TQX Portfolio Tracker

Introduction:

This is the fourth article in the small market effect research series.

The first looked at the holiday effect on SPY.

The second looked at the turn of the month effect, also on SPY.

The third looked at the holiday effect on gas and energy assets

All three sets of research resulted in tradable systems that I have now implemented as overlays on my personal systematic trading portfolio.

If you missed the last one, you can check out the holiday seasonality effect on gas and energy assets here:

In this fourth article, we’re going to examine a market effect with a similar process as before. This market effect is what’s called the Turnaround Tuesday effect.

The basic idea is very simple. Allegedly, Tuesdays tend to be the highest returning day in the market. The claim is that by entering Monday at the close and exiting Tuesday at the close, you can create a simple yet effective trading system.

In this article, we are going to dig into the data to prove or disprove the effect and figure out the most robust way to capture it profitably.

The first half of the article will be a bunch of plots to better understand the mechanics of each piece of the effect. Then, later in the article I will share some system ideas and code to potentially implement into your portfolio.

Note For Paid Members:

As always, paid members get access to the full code at the end of this article.

You also have access to the Discord community where we can discuss this research and ask questions, and the GitHub repo with all published code.

Reason For The Effect:

Before I touch any data, let’s talk about why the Turnaround Tuesday effect might exist in the first place. Because if there’s no real reason for it, then there’s likely no real edge.

The mechanism for the effect is behavioral, and in my view it has three plausible reasons that build on top of each other.

The first and main contributor to the effect is that investors overreact to bad news from the weekend. Between Friday’s 4pm close and Monday’s 9:30am open, there’s a lot of time for bad news to occur. But when that bad news does happen, everyone has to wait until market open on Monday to trade based on the news.

All that accumulated weekend panic hits all at once on Monday morning and produces emotional selling pressure, many times more than there should be. Stocks drop on Monday partly because the bad news is being priced in, and partly because everyone got to sit in their own fears over the weekend and overreacted, thinking the news was worse than it actually was.

The second contributor is what causes Tuesdays to have larger than average returns. Professional and smart retail traders recognize that Monday’s selloff was a big overreaction and step in to buy the dip on Tuesday. They see this as a cheap buying opportunity, as the market has sold off more than it should have. Like most news, it’s almost never actually as bad as it seems. This results in a reversion back to fair value.

The third contributor is shorts covering (this one is the most speculative). Shorts who jumped in on Monday’s weakness may start to cover their positions when the markets revert back towards fair value. This adds mechanical buying pressure right on top of the institutional bids that were buying the dip.

That’s theoretically why this trade should work. There’s no real way to prove it, but it makes sense and is based on human emotion, which is unlikely to ever change.

Research Phase:

Now let’s start breaking down the effect with charts. Each subsection below examines one feature of the effect using the SPY ETF. We will use what we learn about the effect to develop a trading system in the second half of this article.

Baseline Tuesday Returns:

Let’s start with the simplest studies of this effect. Is Tuesday special, or is it just another day of the week? This looks at the baseline effect that the rest of the research will progressively layer onto.

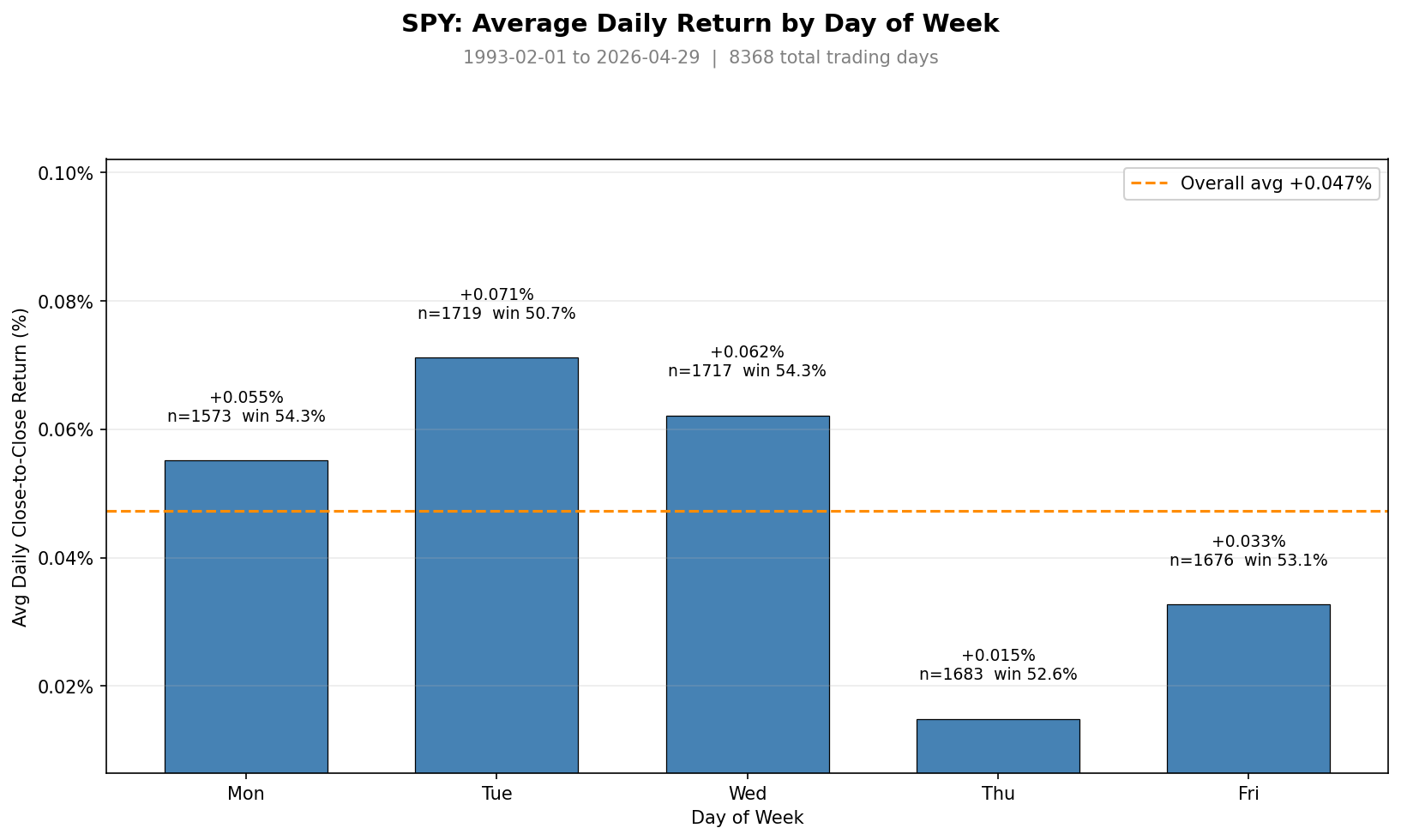

Looking at SPY ETF data from 1993 to 2026, what does the average return look like by day of the week? No filters or regimes, just the raw mean. The chart below shows the average market returns by day of week.

You’ll notice on average over this 33+ year time span, Tuesday wins, but only by a little bit.

Monday: +0.055% return

Tuesday: +0.071% return

Wednesday: +0.062% return

Thursday: +0.015% return

Friday: +0.033% return

Tuesday at +0.071% return is roughly 1.5x the overall SPY return baseline (orange dashed line). Tuesday generally is the best day of the week historically.

But the gap between Tuesday and Wednesday is just +0.009 percentage points, and the gap between Tuesday and Monday is only +0.016 percentage points. So really, at this level this effect is pretty small.

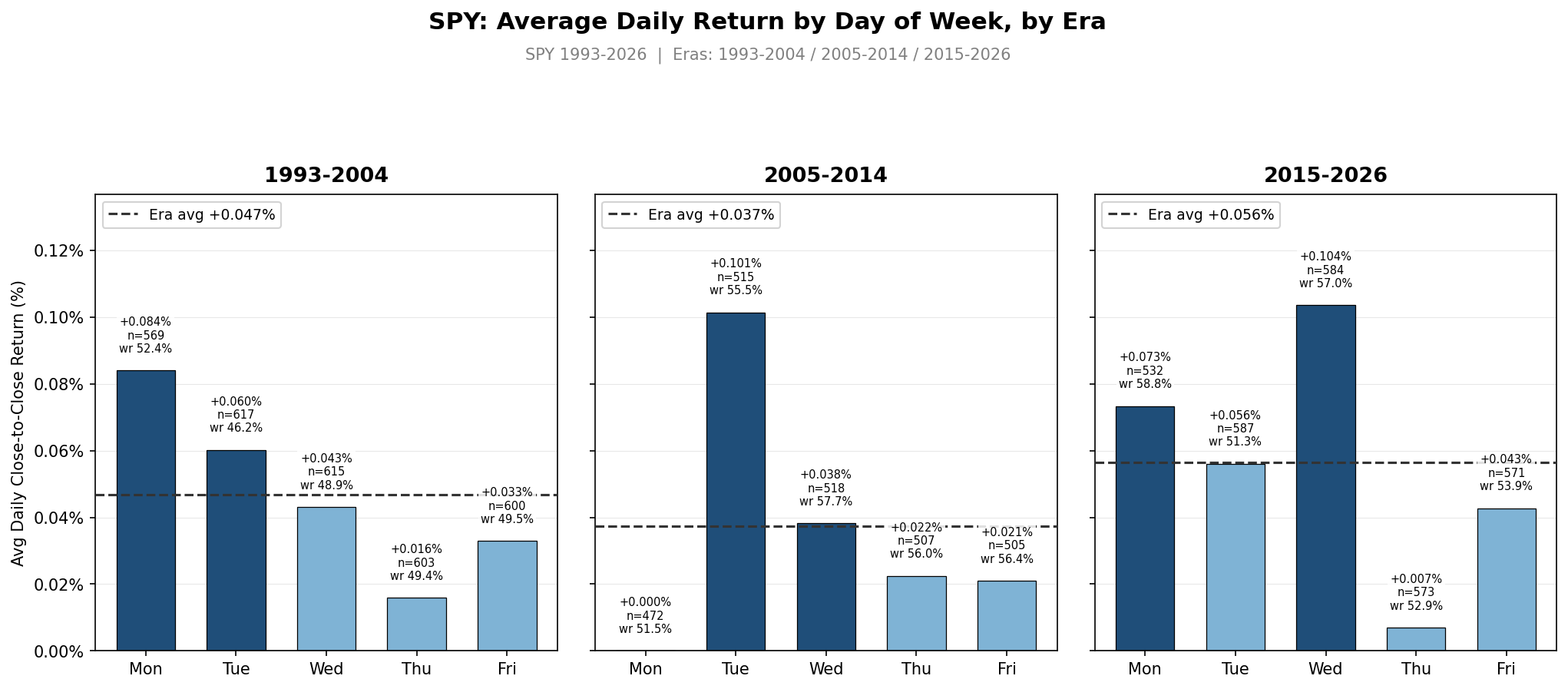

An average result across 33+ years can hide a lot. So, let’s split the sample into three eras and see if the slight Tuesday outperformance is stable or if it’s an artifact of one strong period of history.

Interestingly, you’ll notice the best day of week ranking shifts around.

In Era 1, Monday was the strongest performing day on average.

In Era 2, Tuesday was the strongest performing day on average.

In Era 3, Wednesday was the strongest performing day on average.

The blanket statement that there is some inherent overperformance only on Tuesdays doesn’t seem to hold up. It seems the best performing day shifts around, but appears to be within the first few days of the week consistently, rather than the later part of the week.

This could be just natural noise in the data. Or this could be due to traders getting smarter about when they take advantage of the post weekend sell off, causing the best performing day to shift around. We will never know, but understanding that this effect is a little unstable is still useful information.

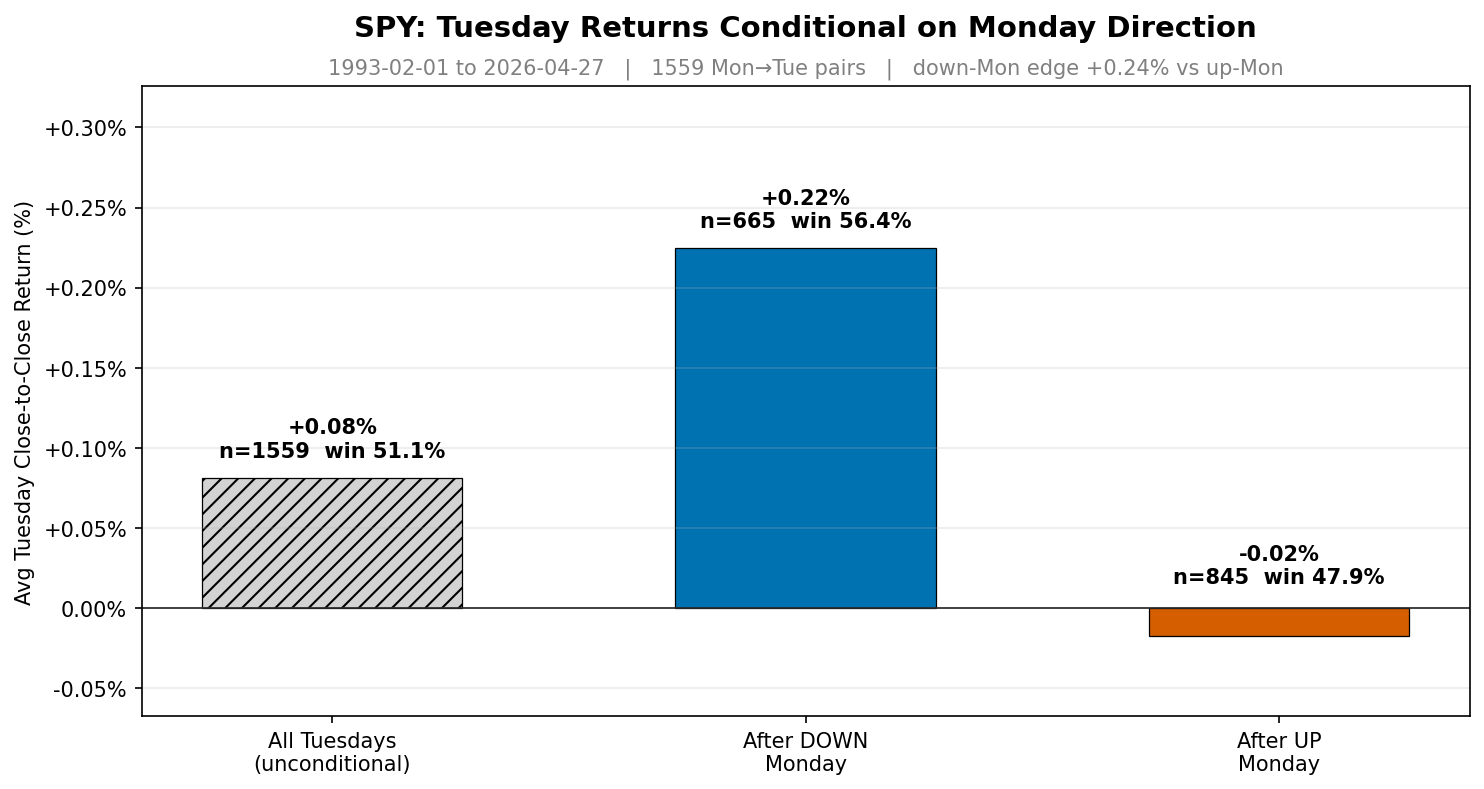

The next thing I looked at was if there was a conditional feature that would predict a larger bounce on Tuesdays. Naturally, it makes sense to try to get a better entry at a lower price to better capitalize on the Tuesday upward swing. Hence, the chart below looks at Tuesday returns as a function of what Monday’s price action did.

You’ll notice that after a down Monday, the Tuesday returns are significantly higher, over 2x the return of just trading every Tuesday. Also, trading Tuesdays after Monday was an up day actually has negative expectancy.

This results in a feature we could add to the system where only trading this effect after a down Monday would result in a predictably higher return on the following Tuesday.

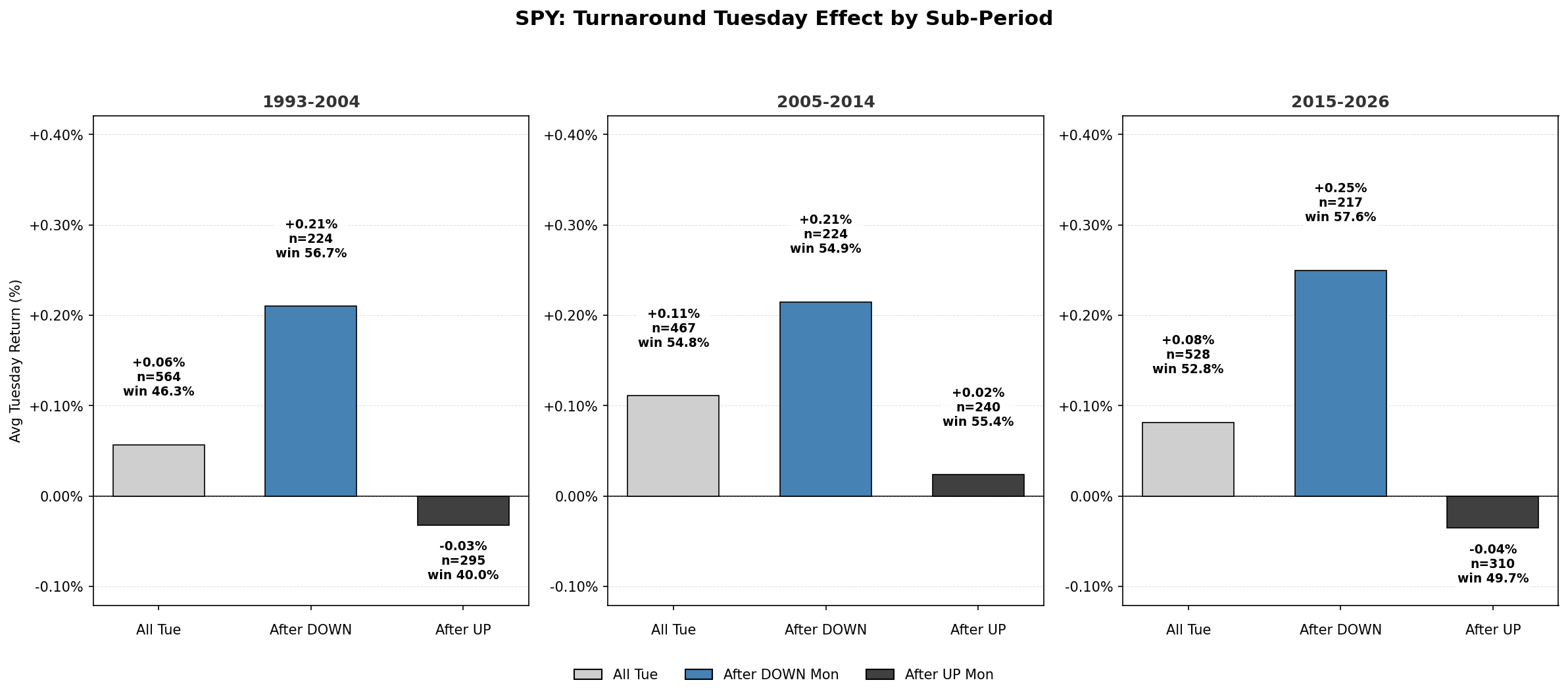

The natural next question is again, does this down Monday feature hold up over time or is it an artifact of some random outliers. Ideally, we want to see this down Monday effect happening consistently over time. The chart below splits the data into three eras to understand time stability.

It appears this feature is stable over time. When Monday is red, the Tuesday returns are significantly higher. And when Monday is green, Tuesday returns are negative or only slightly positive. This Monday red day feature appears to be significant, so in the next section we will explore it further.

Monday-Down vs. Monday Up:

Okay, so the overall Tuesday average return appears to be very small and the best day of the week shifts around slightly over time, but generally stays between Monday and Wednesday. But, when Monday is a red day, it does seem to predictably lead to higher returns on Tuesdays.

This makes sense with the theory behind why the effect exists. Mondays digest all the fear from the weekend, so red Mondays would cause the buying opportunity for large rebounding Tuesdays. If the Monday was green, then no bad news was released over the weekend, and then there was no opportunity to buy the market at an overcorrected discount.

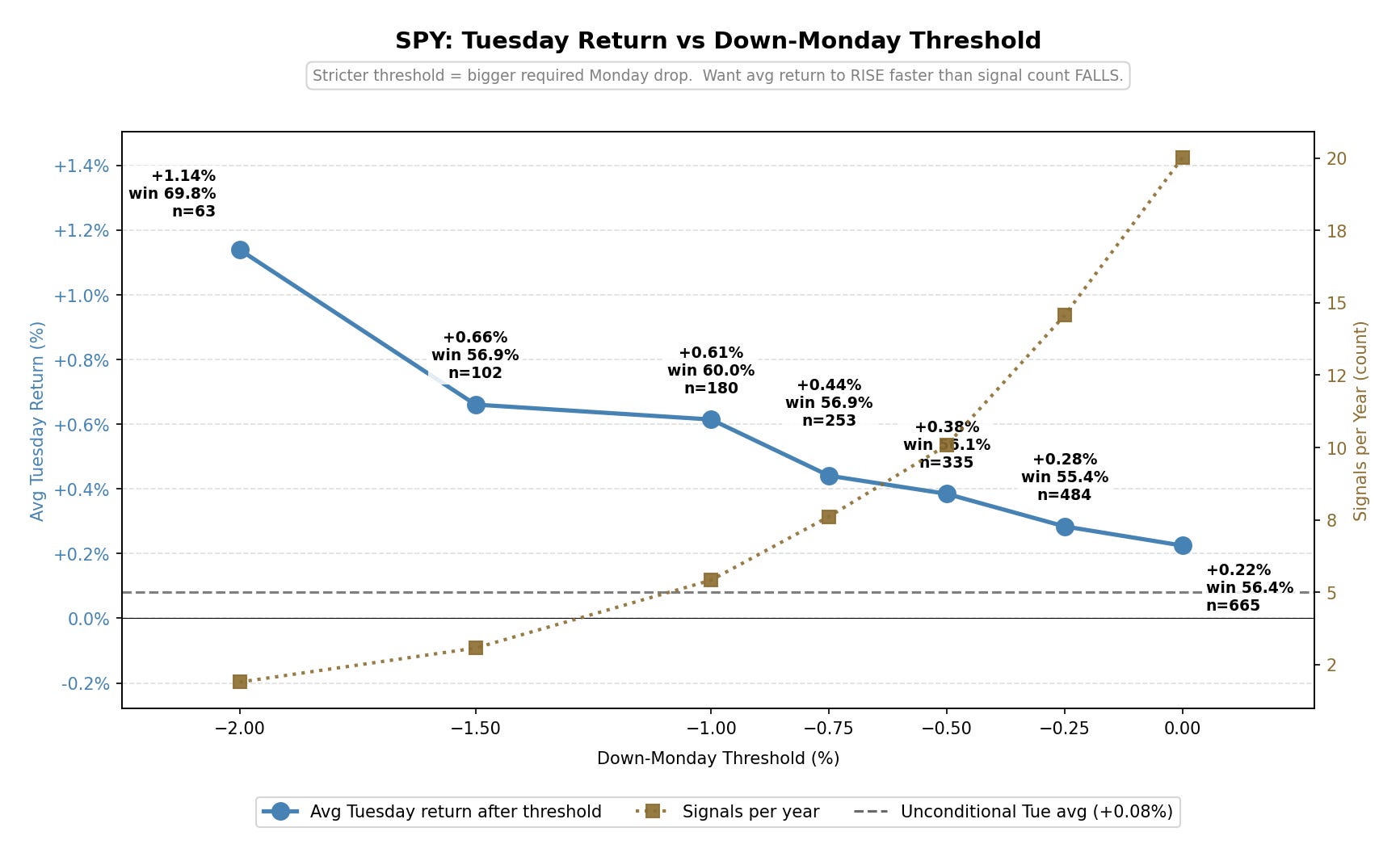

Now, I want to know if the relationship gets stronger as Monday’s drop gets bigger. Is it a binary red vs. green Monday that matters? Or can this signal strength be measured in a monotonic way where larger down Mondays lead to predictably higher return Tuesdays?

The chart below shows that the more Monday sells off, the harder Tuesday bounces.

The further left on the x-axis you go (larger Monday sell offs), the higher the expected return on the following Tuesday. There is a clear relationship here.

We just have to be careful because the more restrictive you are with Monday sell off percentages, the fewer trades you get per year. This would mean fewer data points and less data to make decisions from.

So, while larger down Mondays lead to larger Tuesday bounces, we have to keep in mind that the data points reduce as you go further to the left in the plot.

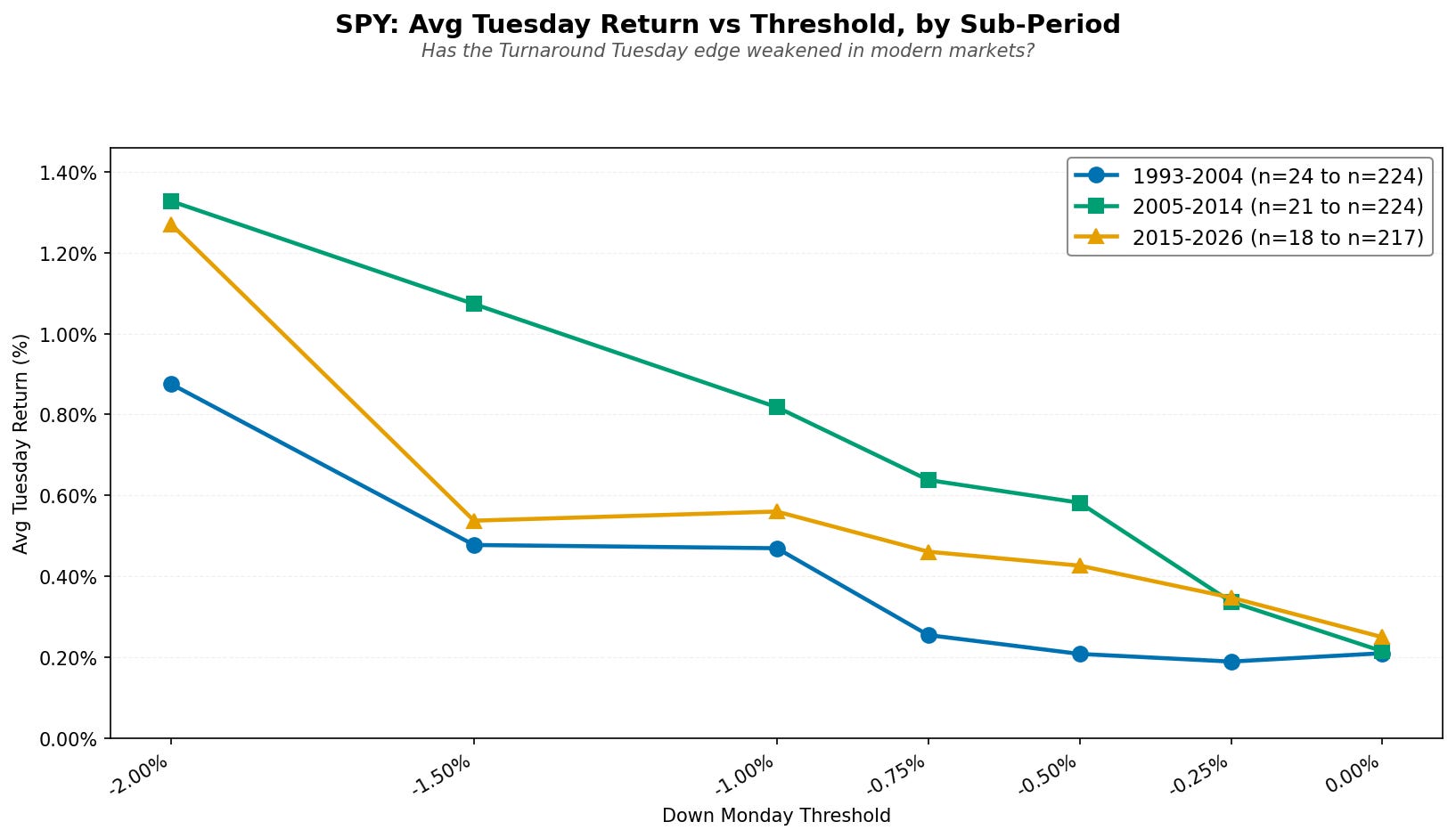

Again, just as the few times before, we want to understand how this feature behaves over time, not just as one blanket average. Below is the same plot as above, just with three lines showing the effect of a larger and larger Monday down day split across the standard three eras.

Across the three eras, we see consistency in this Monday down day feature. This makes me think we can use the severity of a Monday sell off as a way to tune signal strength.

Meaning, have larger position sizes when Monday sold off more and smaller position sizes when Monday sells off less. The data is showing that the strength of Monday’s sell off is predictive of the behavior on Tuesday.

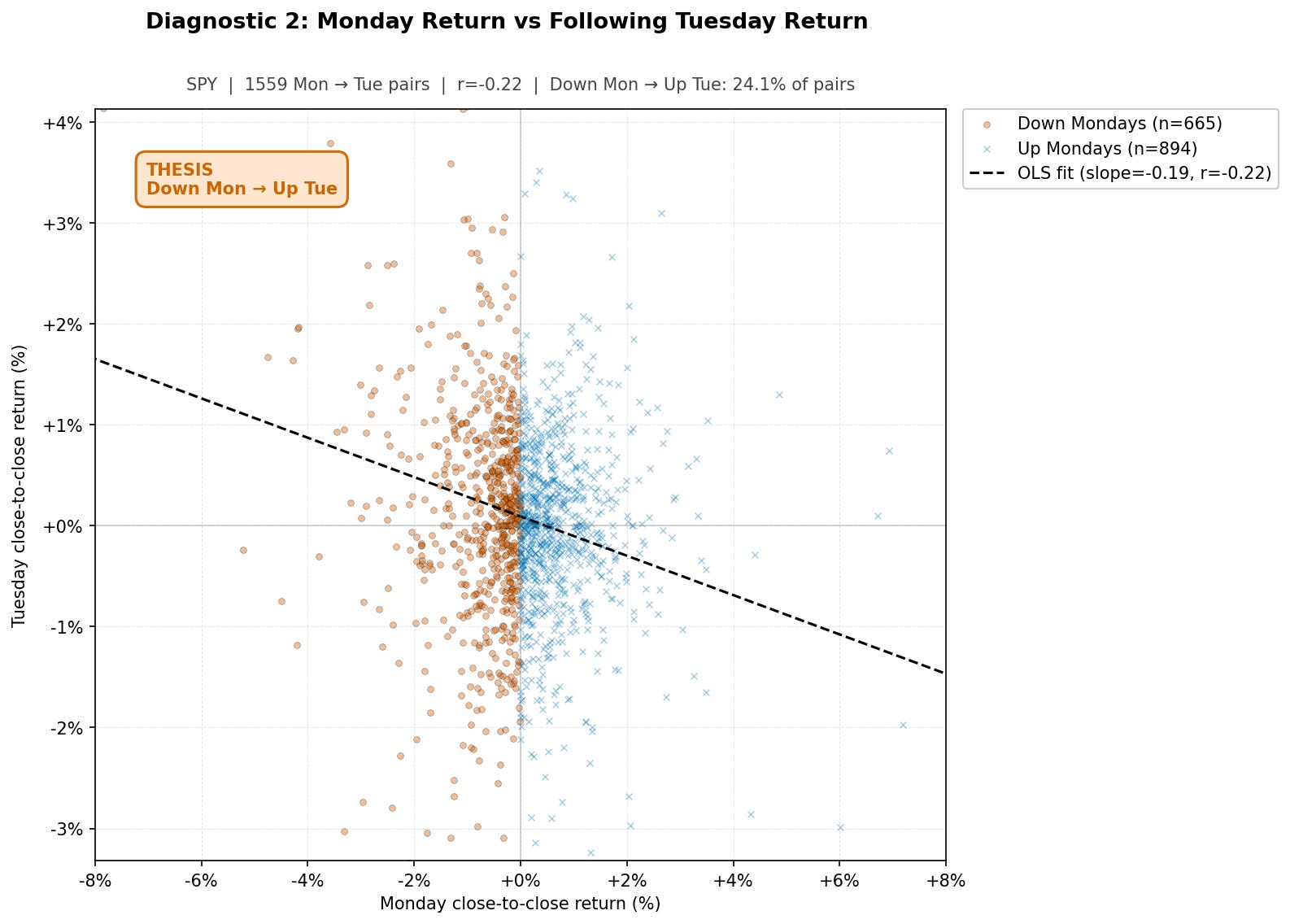

Another way to visualize this is with the scatter plot below. This plot shows the Monday return on the x-axis and the corresponding Tuesday return on the y-axis.

While there are plenty of individual data points that don’t follow the “larger Monday down leads to larger Tuesday up” pattern, the average of the scatter shows this behavior (represented by the sloped dashed black line).

So, the verdict here is that there seems to be some real benefit to using Monday price returns to predict the returns of the following Tuesday.

Now, let’s dig into some more features we can measure to see if they can help us better predict Tuesday’s price return.

Friday-Down vs. Friday-Up:

So far we’ve thoroughly explored Monday being red. But now that part of the effect is understood, I started wondering if there was more historical price data that could be leveraged for more predictive power.

The natural next day to check for predictive power is the previous Friday. If the Monday-down feature is partly about weekend news amplifying selling pressure, then a red (or green) Friday going into that weekend might have some sort of meaning as well.

Basically I want to know:

“Was sentiment going into the weekend positive or negative? And does that matter for this trade?”

A market that’s already selling off going into the weekend leaves traders more nervous over Saturday and Sunday, and that nervousness keeps getting fed by whatever pops up on the news on the weekend. By the time Monday closes red on top of that, the snapback on Tuesday could be even sharper.

That’s the theory anyway.

Let’s see what the data says.

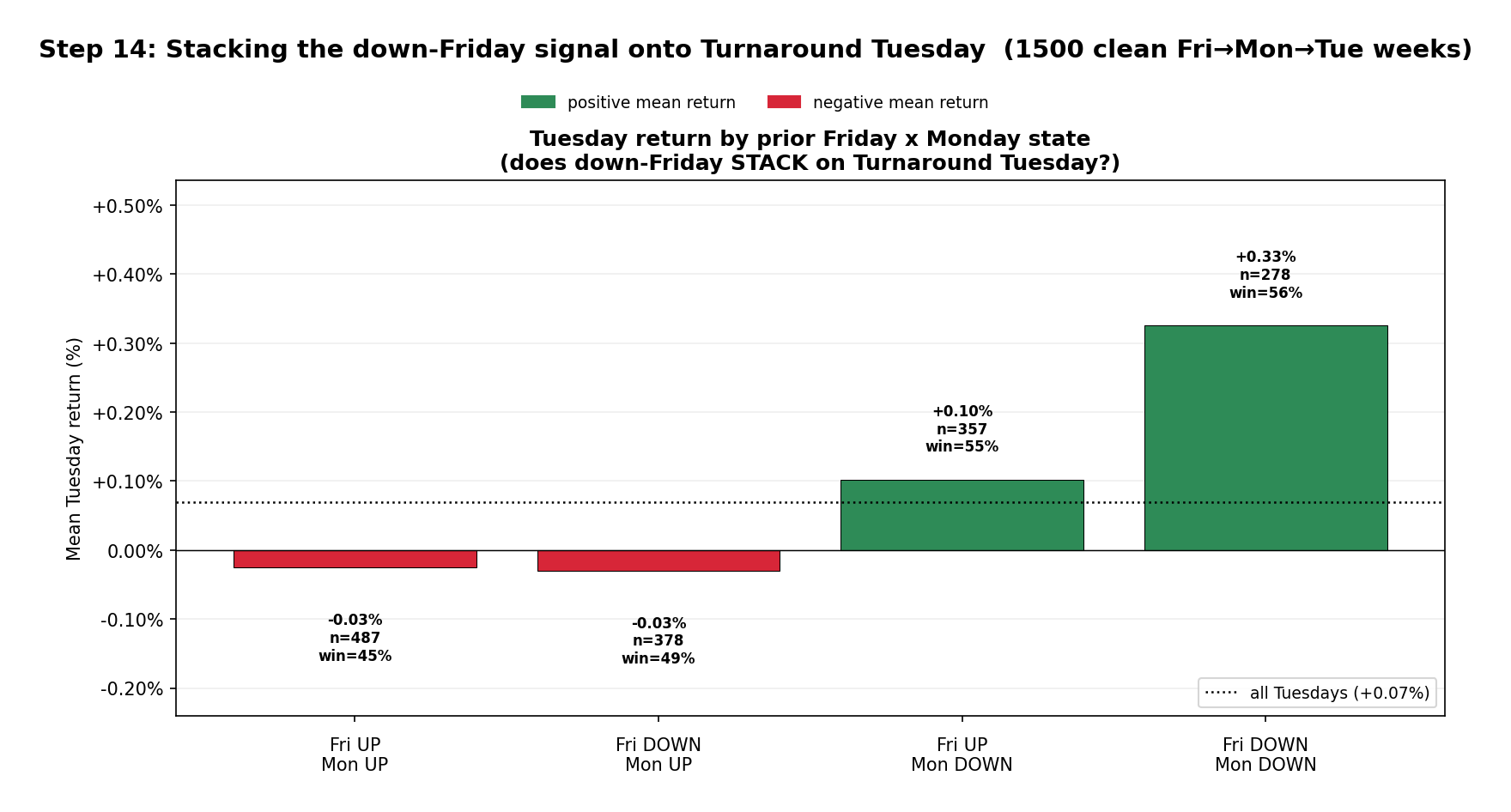

The chart splits the data into the four possible buckets of daily price returns that could happen.

The summary of the result is the following:

Friday up AND Monday up: -0.03% Tuesday average return

Friday down AND Monday up -0.03% Tuesday average return

Friday up AND Monday down: +0.10% Tuesday average return

Friday down AND Monday down: +0.33% Tuesday average return

You’ll notice the two Monday UP bars both result in negative returns (which is consistent with what we observed previously). It doesn’t matter what Friday did, if Monday was an up day, Tuesday returns tend to be negative.

But if Monday was a red day AND Friday was also a red day, the Tuesday returns are amplified even further than when only Monday was a down day and Friday was an up day.

That’s a +0.23 percentage point lift in average returns just from requiring Friday to also be red.

The next question is whether this stacked Monday and Friday down day signal holds up across eras or whether a few data points are skewing this observation.