ETF Mean Reversion Methods: Four Systems Built for the Dip - Part 1

A detailed look at four independent mean reversion entry mechanisms

Welcome to the “Systematic Trading with TradeQuantiX” newsletter, your go-to resource for all things systematic trading. This publication will equip you with a complete toolkit to support your systematic trading journey, sent straight to your inbox. Remember, it’s more than just another newsletter; it’s everything you need to be a successful systematic trader.

Introduction:

I’ve spent a lot of time in the past trying to build mean reversion systems on the entire US stock universe. I figured if I could find that perfect signal, it should work across everything. People say the US is a very mean reverting market, and maybe that’s the case, but I’ve always struggled to develop a system I’ve determined to be robust.

Every single mean reversion system I built would die on recent data. It didn’t matter what signals I used or how I tuned the parameters. I genuinely started to question whether mean reversion even worked on US anymore (Spoiler: it does. I was just looking at the wrong sub-universe).

The breakthrough came when I shifted to ETFs and large cap stocks. The stability was honestly night and day. And once I had that figured out, I didn’t stop at one system. I built multiple independent systems, each using completely different signals to identify when an ETF is stretched to the downside.

In this article, we will cover four of the mean reversion systems I personally trade within my own portfolio. Every system scales into the position across three separate sub-entries, so you’re never fully committed on the first signal. The idea is simple, get the average oversold price instead of trying to guess the exact bottom.

This is Part 1 of a three part series.

Part 1 covers:

The four individual systems

Why ETFs work better for mean reversion (at least for me)

The design philosophy behind the systems

And a detailed walkthrough of each system

Part 2 will cover:

How the four systems combine into a mean reversion mini-portfolio

Discuss a portfolio level system ranking mechanism

Part 3 will cover:

In sample and out of sample validation

Robustness testing

What it actually feels like to trade this mean reversion mini-portfolio live.

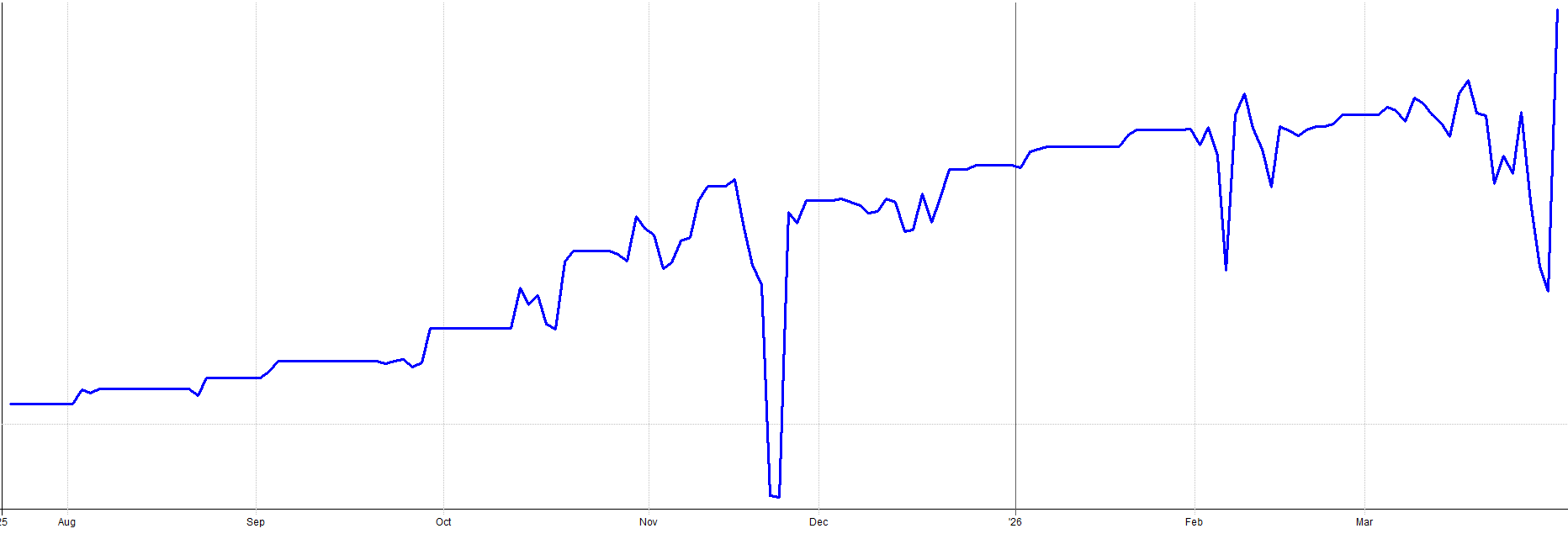

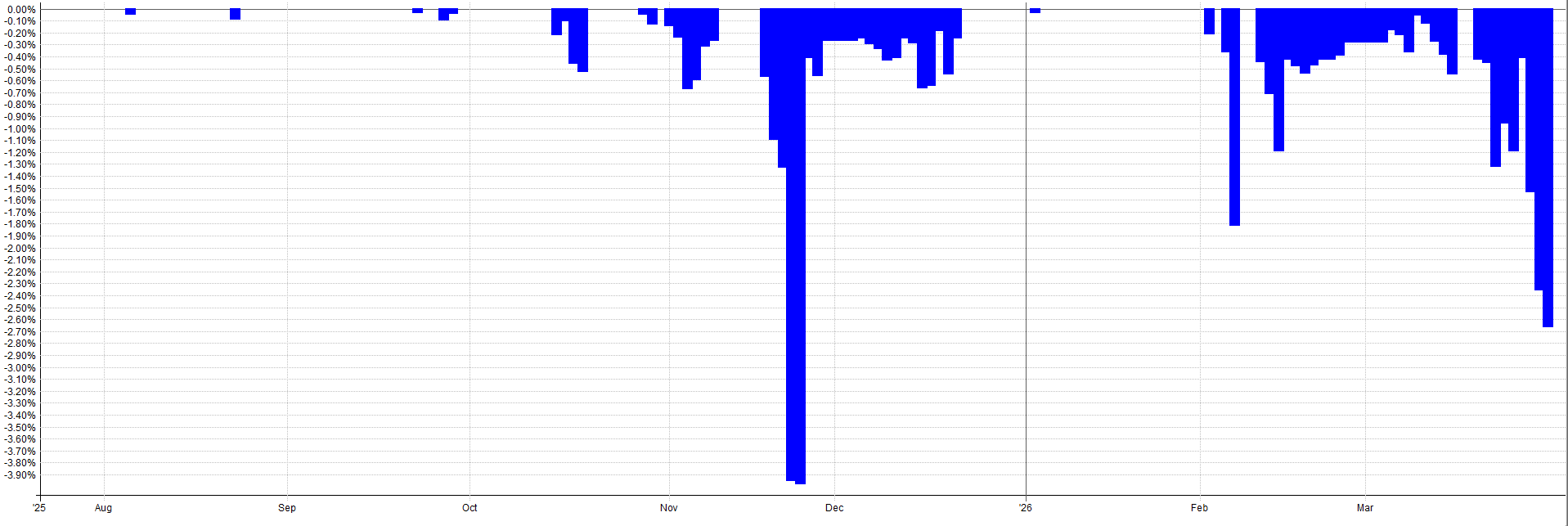

Here’s the combined live performance from my actual live trading account attributed to my mean reversion systems. This equity curve is the combined result of all the ETF mean reversion systems I trade (including the ones shared in this article, along with a few other variants I have).

A little lumpy, a little bumpy, but real results. Being able to take the ups and the downs is just part of the game we play. So far, I’ve been very happy with the performance from these systems which I deployed live in August of 2025.

A Note For Paid Members:

Just before we get into the article, if you are a paid member and have not joined our Discord community, you can do so with the link at the end of the article.

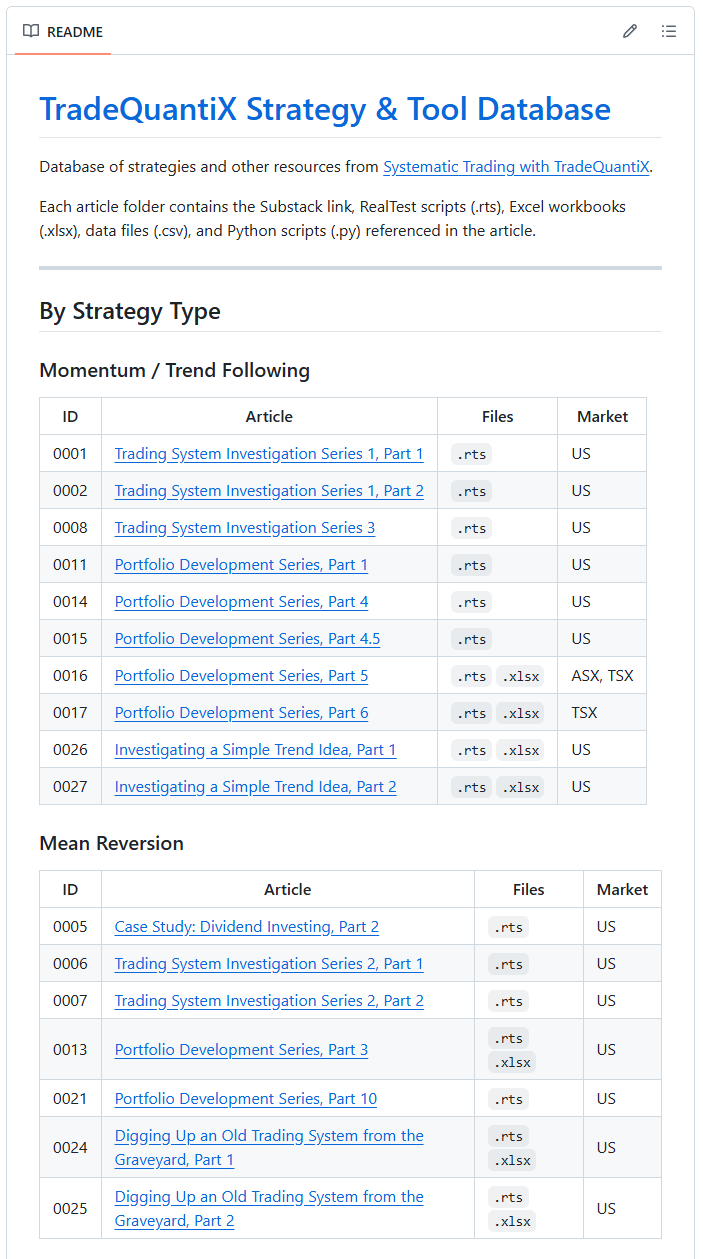

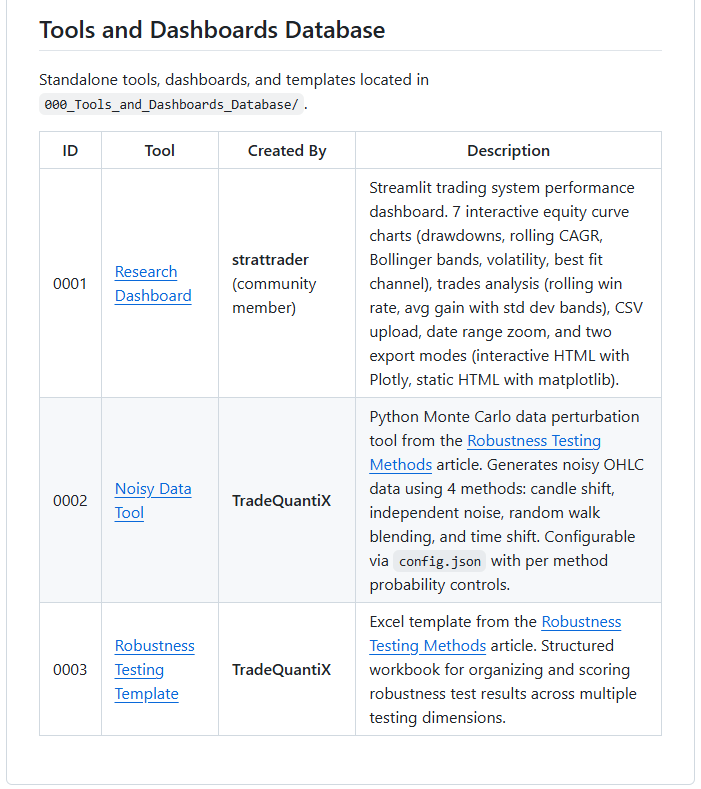

Also, we launched a GitHub to cleanly store all our strategies and tools. When you join the Discord I’ll give you access to the GitHub (or if you don’t use Discord, just message me and I’ll give you GitHub access).

Why ETFs Work Better for Mean Reversion:

ETFs have structural properties that make mean reversion cleaner and more reliable than trying to do the same thing on individual stocks.

The first and most obvious one is there’s no idiosyncratic risk. No earnings surprises, no company specific events, no CEO getting arrested at 2am (the kind of headline that ruins your morning coffee).

When an ETF like SPY drops hard in a day, that drop reflects the entire market or sector selling off. There’s no “oops, they missed earnings by a penny” risk that can destroy the mean reversion trade on instrument you’re holding. Sure equity ETFs are comprised of individual stocks, but that idiosyncratic risk washes out when you go to the index ETF level.

The second reason is a passive flow thesis I have. Large institutional passive flows into major ETFs create a structural bid underneath the price. When the SPY or QQQ dips, the passive bid from retirement accounts, 401(k) contributions, and large funds provide a floor. This is why dip buying in large cap ETFs has been structurally sound for decades.

These equity ETFs are literally created for dip buying and passive flows. The mean reversion mechanism isn’t crowded out because these instruments are designed for mean reversion “buy the dip” type buying.

While large equity ETFs are great for mean reversion properties, ETFs are beneficial in another way too. ETFs can easily give you cross asset diversification. Unlike individual stock mean reversion (which is always equities), ETFs let you easily trade mean reversion across bonds (TLT/TMF), gold (GLD/UGL), crypto (GBTC), and other assets alongside equity indices.

This ease of ETF asset diversification can be leveraged to help build an “All Weather Portfolio” philosophy into the ETF mean reversion systems. This helps to a avoid correlations converging to 1 in a crisis because these asset classes have genuinely different drivers.

This cross asset diversification is extremely important in mean reversion trading because when everything sells off hard and you bought the dip and it keeps dipping, this is exactly when you get hammered from mean reversion. But with some asset class diversification, we can try to mitigate some of that risk because not everything will necessarily correlate to 1 during the next equities selloff.

As a side note, if you’re going to do mean reversion on individual stocks, stick to large and mega caps. These stocks have the institutional backing, rebalancing flows, and retirement accounts trickling in. The same structural bid that makes ETFs work well for mean reversion also exists in large cap stocks. When these stocks hit deep oversold levels, big money comes in to buy the dip. ETF’s like QQQ or SPY are comprised of these large cap stocks, so this structural bid propagates through into those ETFs as well.

On the other hand, small cap mean reversion trading has always been a struggle for me. They don’t have the same structural flows, and when they start selling off, may times there’s simply no big bid to catch them. A stock can just keep tanking because there’s nobody with big bucks stepping in to buy it.

I’ve spend probably 100’s of hours trying to find a mean reversion method that worked for me. Most of those hours were spent trying to make mean reversion work on the full US stock universe. I though that was the only right way to go about it.

It wasn’t until I let myself try different universes and shifted specifically to large caps and ETFs where I finally found some success. The stability was dramatically better, and the reason behind this mechanically makes sense: institutional backing and herd “buy the dip” mentality creates the bounce.

Then, on top of that, I built in an “All Weather Portfolio” like asset class diversification to better diversify the ETF mean reversion mini-portfolio. I’ll explain more about the design philosophy of these systems in the next section.

Design Philosophy:

Before we look at the four individual mean reversion systems, let’s discuss the thought process behind them first. All four systems share the same high level design philosophy, but all four of the systems are measuring mean reversion differently. Below I outline all of the main thought process that went into creating these systems, and why I did what I did.

As you’re reading this section, you’ll probably get a familiar feeling to why I built it the way I did. It takes a similar approach as the concepts discussed in the Luck By Design series:

Why four systems instead of two or six?

As I mentioned, this article will cover four (yes four!) mean reversion systems on ETFs. You may be wondering, why four? Well, that’s because four mean reversion systems will get you pretty dang close to where you want to be.

Going from 0 mean reversion systems to 1 is a big benefit.

Going from 0 mean reversion systems to 4 systems is a massive benefit to your overall portfolio.

After four systems, the increased benefit starts to dissipate. Four I felt was the sweet spot that would give most readers the biggest bang for their buck in their own portfolios.

It’s simply the 80/20 rule applied to a mean reversion portfolio construction. There’s nothing magical about four. It’s just a fantastic starting point (and honestly, four mean reversion systems is way more than most people have).

Ideally, over time you keep adding more mean reversion systems spanning more unique ways to enter, more ways to exit, traded across more ETFs. Four becomes six, becomes eight, becomes twelve etc.

You should think of this the same way you think about any other portfolio. Think of it as something you’re continuously building and adding uncorrelated mean reversion approaches on top of these existing four.

Back to the 80/20 rule, that last 20% of results comes from the next 20 Mean reversion systems you stack on. But that first 80% can be achieved by what I’ll share a little later on in this article.

Multiple independent entry mechanisms.